Ocado Group plc: A dive into the niche world of grocery technology

This post presents a fundamental analysis of Ocado Group (LSE: OCDO), a UK-based grocery retail and technology company, to evaluate its current position and assess its future growth prospects.

Aritra Banerjee

7/24/20259 min read

Ocado Group plc, established in the year 2000 and registered in the United Kingdom (UK), is a pioneering technology company focused on revolutionizing a then niche sector of online grocery retail. In recent years, the company has evolved from primarily servicing the online grocery retail industry to a globally recognized technology solutions provider, leveraging expertise in robotics, artificial intelligence (AI), machine learning, and data-driven automation.

Ocado’s core value proposition is underpinned by two differentiated technology platforms: Ocado Smart Platform (OSP) and Ocado Intelligent Automation (OIA) -

Ocado Smart Platform (OSP): A fully integrated, end-to-end solution tailored specifically for the online grocery sector. OSP combines e-commerce, fulfilment, and last-mile logistics capabilities, offered as a managed service to grocery retailers worldwide.

Ocado Intelligent Automation (OIA): OIA delivers modular, high-performance automation and fulfilment solutions to a range of non-grocery and logistics-intensive industries. It assists businesses in supply chain transformation and solves a variety of industry specific challenges.

In addition to Ocado’s technological solutions, the organization also has two further business lines, i.e., Ocado Logistics and Ocado Retail.

Ocado Logistics: Ocado Logistics delivers third-party logistics services to the group’s UK-based retail partners.

Ocado Retail: Ocado Retail is a joint venture between Ocado Group and Marks & Spencer and is a consumer facing, pure play online grocery business. Ocado Retail serves more than 80% of UK households thereby maintaining a strong footprint in the growing UK online grocery sector.

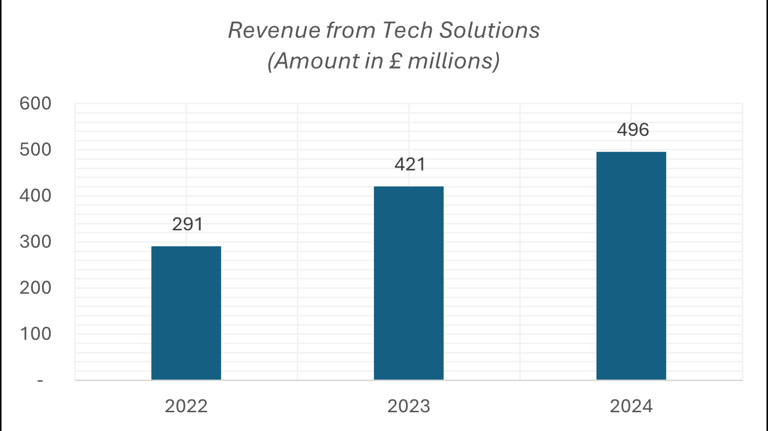

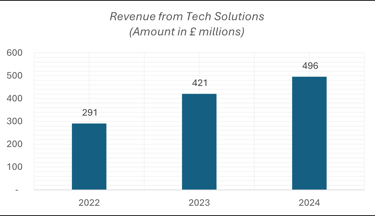

As of FY 2024, Ocado Retail remains the group’s largest revenue contributor, generating approximately £2,686 million, followed by Ocado Logistics contributing £718 million in the same period. Ocado’s technology solutions division, encompassing both OSP and OIA, delivered a revenue of approximately £496 million.

Positive Business Case:

One of Ocado Group’s key value drivers lies in its proprietary technology platforms; OSP & OIA, as mentioned above. Through the continued development of these differentiated solutions, the company is focused on scaling its global technology partnerships and deepening its presence in automation-led supply chain transformation.

Another key differentiator for Ocado is its Customer Fulfilment Centres (CFCs), which integrate robotic arms and autonomous bots to collaboratively pick and pack customer orders with high precision. These bot fleets are capable of processing 50-item orders in as little as five minutes. The CFC technology has significantly reduced the labour time required per online grocery basket from 25 minutes to just 10 minutes. Currently Ocado group has 24 Customer Fulfilment Centres.

Ocado has established strategic partnerships with several leading global grocery retailers, including Aeon, Alcampo, Auchan Retail, Bonpreu Esclat, Coles, Kroger, Morrisons, Sobeys, and Panda, among others.

An organization’s true strength lies in its people, and the same holds true for Ocado. The company’s team of over 2,000 experienced professionals collectively brings around 25 years of specialized expertise in driving transformation across online grocery and adjacent sectors.

Potential Vulnerabilities:

Ocado operates in a highly competitive landscape, facing challenges from traditional grocers such as Tesco, Sainsbury’s, various e-commerce grocery platforms, and technology providers specializing in automation solutions. Sustaining or growing market share in this environment places pressure on margins and requires ongoing investment in innovation.

The organization’s business model is heavily dependent on key strategic partnerships across both its retail operations and technology segment. The termination, non-renewal and underperformance of these agreements could materially impact revenue streams and constrain future growth potential.

Ocado’s core value proposition lies in its advanced automation and logistics infrastructure. Any delays or execution issues in the deployment of these systems for partners could impair its commercial credibility and lead to a loss of future business.

Ocado Group reported a total revenue of £2,686 million in FY24, representing a 5% year-over-year decline from £2,825 million in FY23. This marks a reversal in the company’s topline trajectory, following modest growth of 0.7% in FY22 from 2021, and a significant 12.2.% revenue growth in FY23. The decline in FY24 highlights a notable underperformance relative to recent historical trends, raising concerns around the growth momentum across its business lines.

Ocado Retail, a 50:50 joint venture between Ocado Group and Marks & Spencer, has historically been consolidated into Ocado Group’s financials due to tie-breaking and determinative rights held by Ocado, as outlined in the shareholders’ agreement. These control rights are set to expire in 2024, with Ocado indicating its intention to relinquish control of the JV in 2025. As a result, Ocado will no longer be able to consolidate Ocado Retail’s revenues, which is expected to materially impact group-level topline figures. Beyond the financial implications, the loss of control also signals a strategic retreat from the UK online grocery retail space, a market in which Ocado has been a key player, potentially weakening its consumer-facing presence and competitive positioning in the segment.

Ocado Group has historically struggled to achieve operational profitability, with its core operations remaining in the red despite periodic topline growth. This persistent underperformance is largely attributable to an overall increase in cost, primarily driven by rising depreciation charges, utility expenses, logistics inefficiencies, and labor costs. While revenues grew modestly by 0.7% in FY22 and more robustly by 12% in FY23, these gains were offset by corresponding cost escalations of 8% and 10% respectively, limiting operating margin expansion. Additionally, Ocado Retail has consistently delivered negative EBITDA thereby affecting the group’s consolidated revenue figures. This prolonged underperformance may have influenced management's decision to relinquish control of the JV, signaling a strategic pivot away from the volatile UK retail segment and toward a sharper focus on its technology driven transformation solutions.

Additionally, Ocado’s partnerships has encountered severe headwinds, with key partners such as Kroger (US) and Sobeys (Canada) reportedly slowing or pausing the deployment of Ocado-powered Customer Fulfilment Centres (CFCs). This has contributed to a more muted adoption of OSP technology than initially anticipated by the management, creating uncertainty around the timing and potential returns on invested capital. The capital-intensive nature of CFC development, coupled with protracted ramp-up periods, has further compounded this challenge. These facilities typically require several years to reach optimal scale and utilization, delaying the path to profitability and constraining revenue growth.

Promising Growth Prospects:

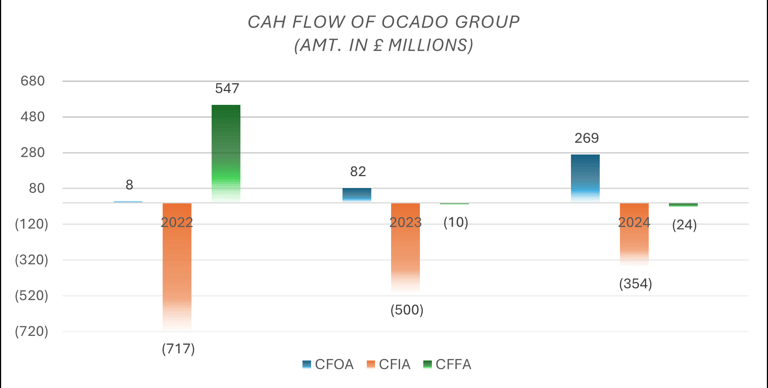

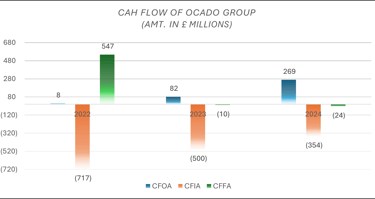

Ocado Group demonstrated a notable improvement in its cash flow from operating activities over its three-year period, rising from £8 million in FY22 to £82 million in FY23 and ultimately to £269 million in FY24. This reflects enhanced operational efficiency, improved working capital management, an improved contribution from higher margin business lines such as technology solutions and the relinquishing of control from loss generating Ocado Retail venture. The sharp increase in FY24 is also attributable to the margin stabilization following prior years of investment and inflationary pressure.

Cash Flow from investing activities remained negative across all three years, declining from an outflow of £717 million in FY22 to £354 million in FY24. The declining investment outflows suggest that Ocado is moving past the peak of its capital expenditure cycle, having completed substantial infrastructure and technology platform buildouts in prior years. This is consistent with the company’s transition from an asset-heavy expansion phase towards monetizing its existing technology and fulfillment capabilities.

Conversely, the cash flow from financing activities saw a sharp swing. After a significant inflow of £547 million in FY22 primarily driven by the issue of share capital to fund heavy investments, the company recorded a net outflow of £10 million and £24 million in FY23 and FY24 respectively. This trend reflects a normalization of capital structure, including repayments of borrowings and lease liabilities, lower dependency on external financing, and potentially limited appetite for new equity issuance.

Overall, the trend suggests that the Ocado group is gradually shifting from a capital-intensive, investment-heavy growth strategy toward a more cash-generative, operationally focused model. The marked improvement in operating cash flows and narrowing investment outflows signal potential for a more sustainable financial profile, though future cash generation may be challenged by strategic changes.

Factors that can negatively influence the group’s operations:

Ongoing geopolitical tensions, including conflicts involving Israel and Palestine, Russia and Ukraine, and rising friction between the US and Iran, have placed considerable strain on global supply chains. These disruptions have contributed to elevated raw material and transportation costs, while also driving up the broader inflationary pressures across key markets. The online grocery retail sector is typically characterized by thin margins, high volume requirements, and significant supply chain complexity. These geopolitical disruptions have the potential to exaggerate these challenges by driving up supply chain and labor costs, thereby placing further pressure on already constrained profitability margins.

The organization primarily serving the online retail sector has been affected by post-pandemic consumer behavioral shift. Majority of consumers have returned to brick-and-mortar grocery shopping, reducing the average basket sizes and the frequency of online orders. For Ocado, this has led to a decrease in the efficiency of CFC delivery density.

Key Performance Indicators (KPI):

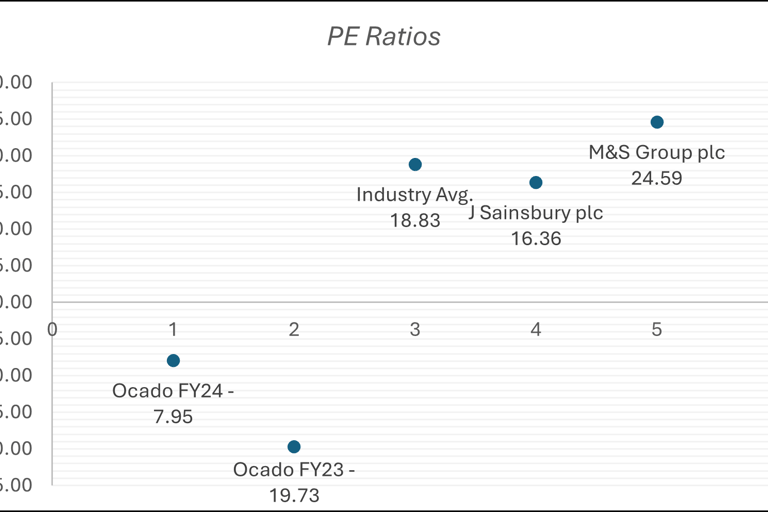

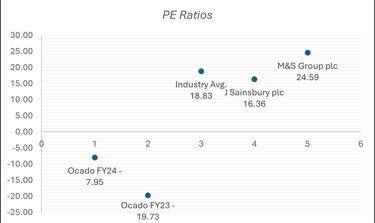

Price to Earnings Ratio (P/E):

Ocado Group has consistently reported negative P/E ratios, standing at -7.95x for FY2024 and -19.73x for FY2023, reflecting the company’s continued inability to generate net or operational profits. In contrast, the broader UK grocery sector maintains a positive sector average P/E of 18.83x, with key players such as Sainsbury’s and Marks & Spencer trading at 16.36x and 24.59x respectively. A negative P/E ratio signals sustained losses, and in Ocado’s case, reflects the ongoing challenges in achieving operational profitability. However, the above scenario is expected to improve as Ocado has undergone a strategic shift by relinquishing control of its loss-making retail venture and focusing heavily on its technological solution offerings. The negative operation results of Ocado also limits the utility of the P/E metric as a valuation tool for the business, and the investor needs to shift their focus towards alternative metrics such as revenue growth, future business outlook, macroeconomic headwinds, and revenue contribution of technology solution business line in case of Ocado, all of which has been discussed above.

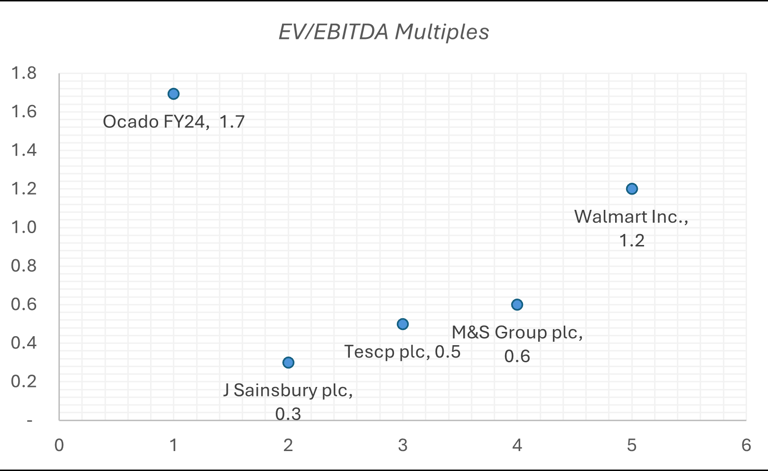

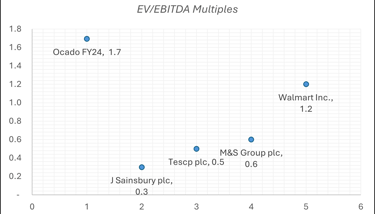

Enterprise Value-to-Revenue (EV/Sales):

In FY2024, Ocado Group recorded an EV/Sales multiple of 1.7x, a level that typically falls within the range considered bullish or potentially undervalued by growth-oriented investors. While this is notably higher than the 5-year average EV/Sales multiples of traditional UK & US grocery retailers, such as Sainsbury’s at 0.3x, M&S Group at 0.6x, Tesco at 0.5x, and Walmart at 1.2x, it reflects Ocado’s position as a technology-driven business rather than a conventional retailer. The elevated multiple may signal investor and analyst’s expectations of long-term scalability, margin expansion, and monetization of its proprietary technology platform, despite current profitability constraints.

Conclusion:

Considering all the factors, we can conclude that the Ocado Group is undergoing a strategic transformation from a capital-intensive online retailer to a scalable, asset-light technology solutions provider. The company is leveraging advanced artificial intelligence and machine learning capabilities to drive operational efficiency, address complex supply chain challenges, and enhance customer confidence. While the long-term positioning appears compelling, investors should remain mindful of short-term headwinds, including elevated operating costs, transition-related execution risks, funding constraints, inflationary pressures, and broader macroeconomic uncertainties.

North America represents a key growth vector for Ocado as it enters quarter 3 of 2025, with the success of its expansion strategy contingent on effective market penetration and disciplined execution of international rollouts. The company’s ability to operationalize its technology solution offerings at scale and deliver margin accretion will be critical in validating its long-term valuation. For patient, growth-oriented investors, Ocado offers a unique “tech-enabled platform” opportunity focused on the retail logistics space with execution and margin expansion as pivotal drivers of sustained shareholder value.

To download the entire report - please click on the "Download Report" button below.

The integration of artificial intelligence is a critical enabler of growth in the grocery and non-grocery logistics sector. For organizations like Ocado, AI plays a central role in enhancing forecasting accuracy, optimizing robotics coordination, streamlining delivery logistics, improving user experience, and supporting strategic planning through advanced simulation. The company has embedded AI across its operations through proprietary technologies such as the OSP, CFCs and OIA, positioning it as a differentiated technology partner to leading global retail players.

Another major technological advancement made by Ocado is the world’s first AI-based fraud detection system for online grocery purchase. Ocado is also leveraging AI & advance machine learning models to combat fraudulent activities in online grocery space.

The last mile part in a supply chain operation, responsible for transporting goods from distribution hubs to end consumers, remains one of the most complex and cost-intensive segments of the entire process. Common challenges include incorrect deliveries, traffic-related delays, and weather-related damage, all of which can erode service quality and customer satisfaction. While this space has traditionally been dominated by major players in the logistics sector such as UPS, FedEx, and country specific postal services, technology providers like Ocado are increasingly deploying AI-driven solutions to address inefficiencies. These include optimizing delivery routes, enhancing delivery accuracy, elevating the end-user experience, and proactively identifying potential disruptions before they materialize.

In conclusion, Ocado Group has executed a strategic pivot from its origins as a pure-play online grocery retailer toward positioning itself as a technology-led transformation partner within the supply chain and logistics space, with a core focus on the grocery sector. This transition is underscored by the company’s decision to relinquish control of the Ocado Retail joint venture and the growing contribution of technology solutions to group revenues. Furthermore, Ocado’s emphasis on embedding AI and machine learning into its operations, along with the development of proprietary, patent-backed technologies, reflects management’s clear intent to establish the company as a differentiated and innovation-driven player in the global technology landscape.